TL;DR:

- Proper revenue recognition requires tracking income earned during the period, not just cash received.

- A structured month-end close, including reconciliation and deferred revenue management, ensures accurate financial reports.

Reporting monthly revenue for a martial arts school means recognizing income earned during the period, not simply recording cash deposits received. The formal term for this practice is revenue recognition, governed in the United States by ASC 606, the accounting standard published by the Financial Accounting Standards Board. Studios that skip this discipline routinely misstate their monthly income martial arts school numbers, which distorts profit analysis and cash flow forecasting. This guide walks you through the accounting prerequisites, the month-end close workflow, and the most common mistakes that cost studio owners real money.

How to report monthly revenue for a martial arts school: prerequisites first

Accurate revenue tracking for a martial arts school starts before the close process begins. You need the right accounting infrastructure in place, or every report you produce will be unreliable.

The first requirement is connecting your payment processors to your accounting software. Platforms like Stripe, PayPal, and Square each bundle multiple transaction types into a single deposit. One deposit can contain revenue, processing fees, sales tax, and refunds, all of which belong in separate accounts. Connecting these processors to QuickBooks or Xero through a sync tool like Synder eliminates manual data entry and reduces the risk of misclassification.

The second requirement is maintaining three subledgers: accounts receivable, deferred revenue, and fees. Deferred revenue is the most misunderstood of the three. When a student pays three months of tuition upfront, that cash is a liability until you deliver the classes. The deferred revenue subledger tracks how much of that prepayment you have earned each month.

Here is a comparison of common tools and what each one handles:

| Tool | Primary Function | Martial Arts Fit |

|---|---|---|

| QuickBooks Online | General ledger, P&L, bank reconciliation | Strong; widely used by small studios |

| Xero | Cloud accounting, invoicing, reporting | Strong; good API integrations |

| Synder | Payment processor sync, deferred revenue | Excellent for multi-processor studios |

| Stripe | Payment processing, payout reporting | Common billing layer for memberships |

Requirement checklist before your first close:

- Payment processors connected to your accounting software

- Chart of accounts includes a deferred revenue liability account

- Accounts receivable subledger reconciled to the general ledger

- Billing cycles documented (monthly, quarterly, annual memberships)

- Refund and discount policies recorded in writing

Pro Tip: Set up your deferred revenue account before you process a single prepaid membership. Retrofitting it after months of deposits is far more time-consuming than building it correctly from the start.

What does the month-end close process look like?

The month-end close is the structured sequence of tasks that produces a reliable financial report for martial arts schools. Skipping steps or doing them out of order causes errors that compound over time.

A target close timeline of 10–15 days after month-end is standard for small businesses. Following a sequenced close process can reduce your closing time to as few as 3 business days, which frees up significant time you could spend on the mat or on marketing.

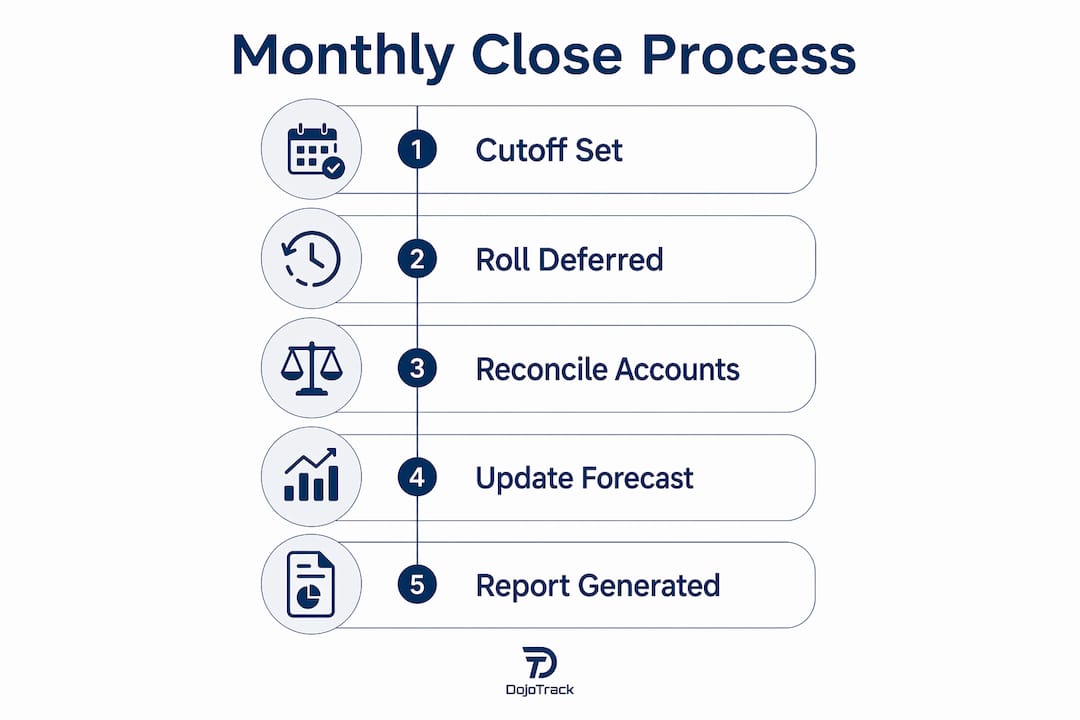

Follow these steps in order:

- Set the revenue cutoff date. Choose a date 2–3 days before month-end. Confirm any deals or enrollments signed in the final 3 days to verify they meet recognition criteria before including them in the current period.

- Roll forward the deferred revenue schedule. Take last month’s ending deferred balance, add new prepayments received, and subtract revenue earned this month. The result is your new deferred revenue liability.

- Reconcile payment processor deposits to the general ledger. Match every payout from Stripe, Square, or PayPal to the corresponding journal entries. Flag any discrepancies before moving forward.

- Post accrual entries. Record revenue earned but not yet billed, such as a student who owes a testing fee not yet invoiced.

- Review the trial balance. Check that total debits equal total credits and that no account shows an unexpected balance.

- Lock the period. Once the trial balance is clean, close the accounting period to prevent backdated entries.

- Prepare the reporting package. A complete management package includes a profit and loss statement, balance sheet, cash flow statement, budget variances, and KPI dashboards. Deliver it by the 15th of the following month.

Here is a summary of the close sequence:

| Step | Task | Output |

|---|---|---|

| 1 | Set cutoff date | Confirmed enrollment list |

| 2 | Roll deferred revenue | Updated liability balance |

| 3 | Reconcile deposits | Matched transaction register |

| 4 | Post accruals | Adjusted journal entries |

| 5 | Trial balance review | Balanced ledger |

| 6 | Period lock | Closed accounting period |

| 7 | Reporting package | P&L, balance sheet, KPI dashboard |

Pro Tip: Build a 13-week rolling cash flow forecast and update it with actual results during each close. Variance commentary alongside KPI dashboards helps you spot trends before they become problems.

How does ASC 606 apply to martial arts school revenue?

ASC 606 is the five-step revenue recognition model that determines when and how much revenue a martial arts school can record in a given month. The model covers contract identification, performance obligation identification, transaction price determination, price allocation, and revenue recognition tied to service delivery. Each step requires judgment, and martial arts schools face specific complexities at nearly every stage.

Here is how each step applies to your studio:

- Step 1: Identify the contract. Each student membership agreement is a contract. The contract defines what you promise to deliver, whether that is unlimited classes, a set number of sessions per week, or access to belt testing.

- Step 2: Identify performance obligations. A single membership may bundle multiple obligations: group classes, private lessons, and curriculum materials. Each obligation may need to be recognized separately.

- Step 3: Determine the transaction price. For a student paying $150 per month, the transaction price is straightforward. For a student who paid $1,500 upfront for a year, you must allocate that price across 12 months of service delivery.

- Step 4: Allocate the transaction price. If a membership includes a free uniform or a discounted testing fee, you allocate the total price across each distinct obligation based on its standalone selling price.

- Step 5: Recognize revenue as obligations are satisfied. Revenue is recognized when earned, meaning when you deliver the classes, not when the student pays. A student who pays in January for February classes generates deferred revenue in January and earned revenue in February.

Applying ASC 606 is judgment-intensive, especially for services like martial arts tuition with prepaid memberships and bundled fees. For a deeper breakdown of how different income sources should be classified, see this guide to martial arts revenue streams.

What are the most common revenue reporting mistakes?

Most martial arts studios make the same errors when they first attempt a formal financial report. Knowing these mistakes in advance saves you from a painful restatement later.

Treating deposits as earned revenue. This is the single most common error. Studios that build monthly revenue from tuition contracts and deferred revenue roll-forwards, then reconcile to deposits, avoid the double-counting that trips up cash-basis thinkers. Cash basis accounting records revenue when money arrives. Accrual basis accounting records it when you earn it by delivering services. ASC 606 requires accrual basis.

Skipping deferred revenue reconciliation. If you never reconcile your deferred revenue subledger to the general ledger, your balance sheet will overstate liabilities or understate them, and your monthly income martial arts school figures will be wrong in both directions.

Missing the cutoff. A student who enrolls on the last day of the month and pays upfront has not yet received any classes. That payment is deferred revenue, not earned revenue. Setting an earlier cutoff date and enforcing it as a control point prevents last-minute enrollments from distorting your period results.

Inconsistent billing cycles. Studios that mix monthly, quarterly, and annual memberships without a documented allocation method produce reports that are impossible to compare month over month. Understanding the impact of automatic vs. cash payment methods on revenue timing is a practical starting point for standardizing your billing.

Accurate monthly earnings for your martial arts dojo depend on one discipline above all others: never let cash timing drive your revenue recognition. Build your reports from contracts and obligations, then reconcile to cash.

Pro Tip: Run a deferred revenue aging report every month. Any balance older than your longest membership term is a red flag that revenue was either recognized too slowly or a refund was missed.

Key takeaways

Accurate monthly revenue reporting for a martial arts school requires accrual-basis accounting, a structured month-end close, and consistent deferred revenue reconciliation tied to ASC 606 performance obligations.

| Point | Details |

|---|---|

| Use accrual basis, not cash basis | Recognize revenue when classes are delivered, not when payment arrives. |

| Maintain a deferred revenue subledger | Track prepaid tuition as a liability until the service period is complete. |

| Follow a sequenced month-end close | Complete cutoff, reconciliation, accruals, and trial balance in order every month. |

| Apply ASC 606 to every revenue stream | Allocate transaction prices across all performance obligations before recognizing income. |

| Deliver reports by the 15th | A complete P&L, balance sheet, and KPI dashboard by mid-month supports faster decisions. |

Why revenue discipline is the real competitive advantage

Here is the uncomfortable truth we have learned from working with martial arts studio owners across the country: most owners know their bank balance but not their actual monthly earnings. Those are two very different numbers, and confusing them is what keeps studios stuck.

When you close your books accurately every month, something shifts. You stop reacting to cash flow surprises and start forecasting them. You can tell a prospective investor or lender exactly what your studio earned in the last 12 months, broken down by membership dues, testing fees, and retail. That kind of clarity builds credibility that no marketing campaign can replicate.

Faster closes also free up real time. A studio that completes its close in 5 days instead of 20 has two extra weeks per month to focus on curriculum, student retention, and community events. The accounting discipline is not the goal. It is what makes the goal possible.

We also believe that standardized revenue reporting is the foundation of a scalable martial arts business model. Without it, you cannot benchmark performance, identify your most profitable revenue streams, or make confident decisions about adding locations or instructors. The studios that grow are the ones that treat their financial reports as a management tool, not a tax obligation.

— DojoTrack

How Dojotrack makes monthly revenue reporting easier

Dojotrack is built specifically for martial arts studios, which means its reporting tools reflect the way your revenue actually works. The platform syncs directly with Stripe to pull payment data into organized reports, separating membership dues, testing fees, and retail sales automatically. Deferred revenue is tracked at the membership level, so your month-end close starts with clean data instead of a spreadsheet full of manual entries. Use the lifetime value calculator to project membership revenue and stress-test your forecasts. If you are switching from another platform, easy data migration means your historical revenue data moves with you. Explore the full Dojotrack platform to see how automated reporting fits into your daily operations.

FAQ

What does “report monthly revenue” mean for a martial arts school?

Reporting monthly revenue means recording the income your school earned during the month by delivering classes and services, not just the cash you collected. This follows accrual basis accounting and ASC 606 revenue recognition standards.

What is deferred revenue in a martial arts studio context?

Deferred revenue is prepaid tuition or fees that a student has paid but that you have not yet earned by delivering the corresponding classes. It sits as a liability on your balance sheet until the service period is complete.

How long should a martial arts school month-end close take?

A well-sequenced close process can be completed in 3–5 business days. The target is to deliver a complete management reporting package, including a P&L and KPI dashboard, by the 15th of the following month.

Why can’t i just use cash deposits to report monthly income?

Cash deposits bundle revenue, fees, sales tax, and refunds into a single figure. Relying on deposits alone leads to double-counting and misstatement. You must reconcile deposits to your general ledger and deferred revenue schedule to produce an accurate report.

Does ASC 606 apply to small martial arts schools?

ASC 606 applies to all U.S. businesses that enter into contracts with customers, regardless of size. For martial arts schools, it governs how and when you recognize membership dues, testing fees, and prepaid tuition in your monthly financial reports.